Probability of default in Euro junk bond is now in the ranging of [-0.02, 0.01].

Yep, apparently accordingly to the bond calculation, you can go negative on default rate (basically implies junk debt will never ever and ever default and more, whatever “more” means in this scenario). There’s probably a reason why they are called “high-yield” or “junk” debt in the first place or not? For one in general, operating cash flow is starting to hit its limit in terms of liability financing, and balance sheet cash is starting, if not already, has been tapped to serve these liabilities.

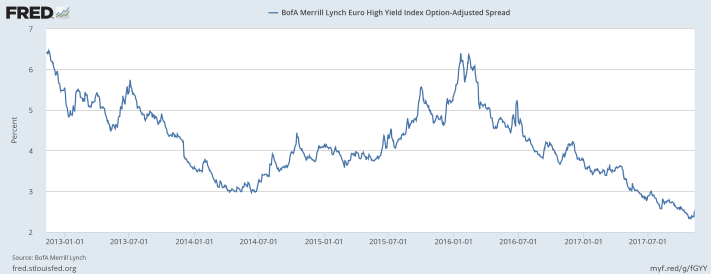

Investors price European junk debt as too safe to fail, thanks to funky bond math. US Treasuries is now trading at a premium over Euro junk bond for some quarters now. Even though US and Euro high-yield spreads have wide substantially in the past 1-2 weeks alone relative to past year or so, risk premium is still really tight by decades-long perspective.