Throughout my work and school, I learned several methods of property valuation. Estimating the value of a property is important because it provides the framework and foundation for a variety of endeavors, including real estate financing, investment analysis, tax and property insurance. Bear in mind that regardless of how “accurate” the valuation is, it does not guarantee you will make income and property appreciation in perpetuity. There are three different valuation methods utilized by the majority of professionals: Income Capitalization, Comparative Market Analysis, and cost approach.

1) Income Capitalization

Income Capitalization involve the use of capitalization rate. This is very similar to the most-basic valuation of a stock where stock value (v) = Dividend/ (r-g) (also known as the Gordon Growth Model). Cap rate for property valuation is similar in that the property value = rental income/cap rate or cap rate = rental income/property value. Rental income should be annualized and the 2-3% yearly inflation is not accounted for.

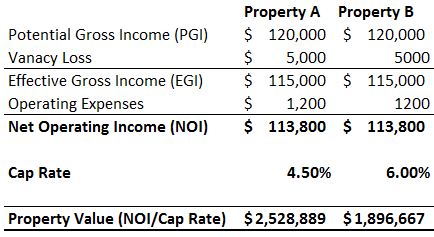

- Estimate the annual potential gross income (PGI). This data is usually derived from the rent of previous tenants (if the building was occupied before) or surrounding neighbor’s rent (if it’s a new building). Most investors usually discount or add a premium to this rent data. For example, an investor might want to build a community pool for a group of condos, thus annual fixed maintenance fee must be taken into consideration). Room/building vacancy is the next criteria to take off from the PGI. PGI – vacancy loss = EGI (effective gross income).

- EGI – operating expenses (i.e. maintenance and gardening fee etc.) equals the net operating income (NOI). NOI/ cap rate = value of the property.

- Cap rate is usually derived from comparables from the surrounding property market. For example, a Class A building in downtown Seattle might have a cap rate of ~4.5%. Investors can also discount or add a premium to the cap rate b/c it will change the property valuation.

- Example: As the example demonstrates below, the cap rate will derive different property valuation for the same property.

2) Comparables

o This is also known as comparative market analysis. Similar to comparable analysis for equity and debt, properties with similar quality, size, features, and location (proximity to school and transportation) etc. should have similar price. This approach is pretty common and easy to use amongst appraisers. The downside to this valuation is that your dataset might be based on a frothy valuation.

3) Cost Approach

o This approach analyzes the valuation of the land and building separately. For example, if an investor is buying a building with poor conditions, but the land the building on is of great value, then the investor will have to calculate the price of the land, cost of taking down the old building and putting a new one on the land. Deprecation will be taken into consideration for this approach.